Early tallies of 2015 participation in the Affordable Care Act exchange are bound to raise follow-up questions, not only among those who doubt anything President Obama says but those trying to sort out the nuances of a complex system.

The White House was eager to announce a preliminary estimate of 11.4 million sign-ups nationwide. That includes totals from the 37 states that use the federal marketplace as well as "preliminary analyses" of data from state-run markets. Federal officials say that number is 10 percent over the White House target, with numbers that jumped significantly in the final week.

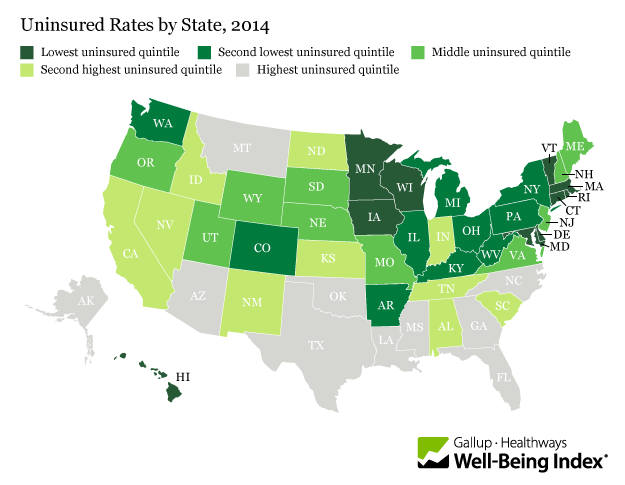

|

| White House graphic touting tally |

As indicated by the "preliminary" label, that tally is bound to change. Some states that run their own markets have granted extensions to the Feb. 15 deadline because of winter storms or system glitches. Some who hit snarls in the federal exchange on the final weekend got an

extra week to finish enrolling.

The tally includes people who selected plans but won't actually pay the premiums. Kevin Counihan, CEO of the federal marketplace, predicts that about 87 percent of enrollments will translate to actual coverage. That comes to about 9.9 million people. Obamacare critic

Avik Roy noted that 2014 ACA retention translated to 84 percent, "fairly similar to (the rate) experienced by private insurers in the conventional ... insurance market."

The feds also released totals for the states using HealthCare.gov and major cities within those markets (

read that report here). We don't yet have a breakdown of new plans vs. renewals for the states, though Counihan said about 8.6 million of the 11.4 million nationwide, or 75 percent, were renewals. Nor do we have a final count on how many got subsidies, though

a Feb. 9 report pegged North Carolina's total at 92 percent.

Katherine Restrepo, health analyst for the

John Locke Foundation, notes that while that percentage may be accurate it can be misleading. Those at the high end of eligibility (up to $95,400 for a family of four) get small tax credits that do little to lower costs, she says.

Roy contends that the White House tally is "deceptive" because it includes an unknown number of people who already had insurance and switched. It's true that the totals don't distinguish between those who had insurance and those who didn't, though I'm not convinced that the White House and "friendly media outlets" have claimed otherwise.

Finally, reader Bryan Griffith correctly called me out for not including any specifics in

a recent article citing a surge of last-minute enrollments in Charlotte. Here's what the latest report shows: The Charlotte metro area got almost 17,000 sign-ups between Feb. 6 and Feb. 15, or about 12 percent of the total enrollment logged during the 13-week enrollment period.