By reining in tax deductions for insurance executives' salaries, the Affordable Care Act brought in at least $72 million in additional revenue in 2013, according to a study by the Institute for Policy Studies.

The tax change is designed to help pay for increased health insurance coverage, which is expected to cost the federal government $36 billion this year. The ACA, commonly known as Obamacare, limits health insurance companies to deducting $500,000 per executive as a business expense. For most companies the cap is $1 million, but the deductions can run much higher when compensation is classified as performance pay.

By requiring individual coverage and offering federal subsidies, the ACA boosted the customer base for insurance companies.

By requiring individual coverage and offering federal subsidies, the ACA boosted the customer base for insurance companies.

The Washington-based IPS, a social justice think tank that strives to "challenge concentrated wealth and corporate influence," analyzed SEC filings on executive pay at the nation's 10 largest insurance companies. The group found that the loss of the tax break didn't lead to a reduction in executive pay, but did mean the companies had to pay more taxes.

"In 2013, the 10 health insurance corporations we analyzed paid their top executives a total of nearly $300 million in taxable compensation. If the Affordable Care Act had not been in force last year, these corporations could have claimed as much as 96 percent of this compensation — $289 million — as deductible 'performance' pay," the report says.

The actual increase in tax revenue is greater when smaller companies are factored in and is expected to grow in coming years, the report says.

Authors Sarah Anderson, Sam Pizzigati and Marjorie Elizabeth Wood advocate for expanding the cap: "If the Obamacare executive pay tax provision applied to all major U.S. corporations, not just to health insurers, U.S. taxpayers would save $50 billion over the next 10 years — and deliver a major blow against CEO compensation business as usual."

Thursday, August 28, 2014

Study: ACA tax on insurance-exec pay nets $72 million

Wednesday, August 27, 2014

Connecticut exec named CEO of federal marketplace

Kevin Counihan, CEO of Connecticut's insurance exchange, will take the same post managing the federal exchange set up under the Affordable Care Act, the U.S. Department of Health and Human Services announced Tuesday.

That puts him in charge of North and South Carolina's subsidized health insurance programs as well, since state officials declined to set up their own marketplaces.

|

| Counihan |

Counihan has worked in health care and insurance for three decades. He oversaw Connecticut's creation of an exchange that signed up about 79,000 people.

The challenges of his new job are plentiful, Jeff Cohen of WNPR and Diane Webber of Kaiser Health News report: "Healthcare.gov serves states that are actively hostile to the law in the Deep South, states that are embracing the law to some minimal degree and states that are active partners in running the exchange."

Tuesday, August 26, 2014

Mandatory calorie counts still stalled

Until this week, I've never thought of the Affordable Care Act when I choose nuggets over the Chik-Fil-A sandwich.

|

| 170 calories more than nuggets |

The latest post from the Food and Drug Administration forecasts that rules will be ready at the end of 2014, taking effect six months later for restaurants and a year later for vending machines, "although input on these effective dates is welcome."

Mandatory nutrition information is part of the push to make us healthier in ways that go beyond providing insurance and encouraging preventive medical care (depending on your political perspective, it may also be another sign of government meddling in private business and personal choice).

Will it work? The evidence so far is based on the growing number of restaurants that voluntarily display calories. Marion Nestle's Food Politics blog steered me to a recent U.S. Department of Agriculture study which found, not surprisingly, that people who have healthier eating habits to start with are more likely than others to notice and use that information.

As a woman who keeps fresh vegetables at home and tries not to rely too heavily on eating out (FAFH, or food away from home, in USDA parlance), I fit the profile of someone who benefits from visible calorie counts. I also illustrate what Duke researchers concluded last year: It helps to have the information in advance, rather than see it for the first time when you walk in hungry (see Karen Garloch's round-up of that and other research on the topic last summer).

I did Weight Watchers several years ago, when it was harder to find the calorie, fat and fiber data needed to calculate points. After searching the internet I was stunned to learn how fattening many of my restaurant meals were, even when I thought I was going light. I narrowed my list to a very few options with reasonable calorie counts for someone of my age and activity level. One was eight Chik-Fil-A nuggets (270 calories), a fruit cup (50) and unsweet tea.

|

| 540 calories? Aww ... |

But it seems my vision can also be selective. I frequently use calories on the Panera menu to choose a meal, but until this week I'd have sworn they weren't listed for pastries. I took a close look on my afternoon coffee walk, and yikes! I guess those 410-calorie chocolate pastries and 540-calorie orange scones need to stop following me home.

Monday, August 25, 2014

Is there an iPhone in the house?

Can you really use your phone to check your heartbeat and find out whether it's healthy? That caught my attention when I heard a report on medical apps on WFAE last week.

Just a few days earlier, speakers at the Charlotte Chamber's health care summit had talked about the huge number of health-related apps on the market and the likelihood that technology will play a growing role in consumer-driven health care. The idea is that as regular people foot a larger share of the costs, they'll rely more on technology to make decisions about medical needs and how to spend their money.

But I hadn't really grasped that my phone and tablet could be used for more than looking up information -- or that health apps could be more than a fun gizmo to encourage fitness.

The recent Marketplace report by Lauren Silverman highlighted the increasing number of apps being marketed to diagnose serious conditions, from macular degeneration to rheumatoid arthritis, and the debate over how to monitor them. "Regulators are walking a fine line between letting snake oil salesmen roam free and discouraging legitimate developers," she reported.

The law professor who was quoted about using an app to record heartbeat and bowel sounds sounded a note of warning against letting apps substitute for real medical care. The Food and Drug Administration reviews only the riskiest apps, Silverman reported.

I'm healthy enough not to need much monitoring, and old-school enough that if I want to hear my heart or digestive system I get out my father's stethoscope. For those of you exploring the frontiers of smartphone health care, what are you learning?

Thursday, August 21, 2014

Workplace insurance: Bad news and good

If Walmart turns out to be a trendsetter, the Affordable Care Act may be driving up the number of people who have workplace insurance, New York Times writer Margot Sanger-Katz reports.

|

| Sanger-Katz |

Wednesday, August 20, 2014

Ex-doctor, now 'navigator,' launches Obamacare blog

John Scherr isn't your typical Obamacare volunteer.

Nor is he your typical doctor, medical administrator, small business owner or individual insurance customer. It's his combination of experiences that led the recently retired Charlotte physician to create a blog that delves into the potential and problems of the Affordable Care Act.

|

| Scherr |

Scherr says he's been interested in ways to rein in health care costs since his days in a private internal medicine practice in Atlanta in the 1980s, when HMOs were the rage. He volunteered to take part in one of the early "capitation" contracts, in which doctors are paid by the patient, rather than collecting a fee for each office visit, procedure and test.

About 20 years ago, he was part owner of a business with about 100 employees. There, he says, he learned the challenges of huge annual premium increases, which often meant switching providers and forcing employees to change doctors.

When he came to Charlotte, he worked as a hospitalist (a doctor who sees patients only while they're in the hospital) for Carolinas HealthCare System and got involved in administration of that group. And when he started thinking about retirement, he got an eye-opening look at what it would cost to buy his own insurance, an experience he writes about in a post titled "Obamacare and Me." This year he helped his two adult daughters buy insurance policies on the federal exchange created by the Affordable Care Act, and that's where he expects to get his own insurance (without subsidy) in 2015.

Scherr recently took the 30-hour training to become an ACA health insurance navigator; he has started volunteering with the nonprofit Enroll America. He's tapping that experience for a series of posts on the twists and turns of our nation's health insurance revolution.

A self-described liberal Democrat, Scherr writes that he was deeply disappointed by the compromise that won Congressional approval, modeled largely on conservative plans. But he says his interest now is on getting past the political rhetoric of the left and right to explore the reality of what's happening and what's to come. He writes that he sometimes feels like a Republican as he learns to value the free-market competition between insurance companies: "This competition will encourage, for the first time, health insurance companies to lower medical costs. If they have lower costs, they will be able to offer lower premiums, and thus receive a higher market share. ... All that’s needed now is to get Amazon involved in the health insurance delivery business, and the problem will be solved entirely."

Scherr says he hopes his blog will help people understand how to get better, less costly health care. He'd also like to encourage policymakers to join him in open-minded exploration.

"Republicans just want to vote to repeal the law, and Democrats don’t want to admit that there is anything in the law that needs to be changed," he writes. "There is more than enough blame to go around, and there are plenty of improvements that need to be made. Hello, Congress? Pay attention to your constituents! Get it together and do your job! Debate, argue, defend, parry – but at the end of the day, COMPROMISE and come up with some solutions that are not so fundamentalist in nature that only the hard-wingers on both sides are heard."

Tuesday, August 19, 2014

98,000 uninsured in NC could qualify for help

Almost 98,000 uninsured North Carolinians may qualify for special enrollment that could get them subsidized health insurance, according to estimates released today by the nonprofit Enroll America.

The 2015 open enrollment period for Affordable Care Act insurance exchanges doesn't start until Nov. 15, but life changes such as marriage, moving or losing a job spark 60-day special enrollment periods.

The federal government hasn't released any numbers on how many have actually taken advantage of that option, but Enroll America used Census data to estimate the percent of each state's uninsured population likely to experience a move, marriage, birth or new citizenship in the seven months between 2014 and 2015 open enrollment.

In North Carolina that would come to 6.9 percent of more than 1.4 million uninsured, or 97,905 people. In South Carolina the group estimates that 47,850 people, or 6.8 percent of the uninsured population, experienced one of those changes.

The report also says almost 52,500 people in North Carolina and 29,650 in South Carolina are likely to be released from incarceration or earn permanent resident status during that seven-month stretch. Those events also trigger special eligibility.

Monday, August 18, 2014

Sneak peek at 2015 rates? Not in NC

When I started covering the Affordable Care Act recently, the folks at Families USA urged me to write about public review of proposed health insurance rates for 2015. Several states require companies to post their rates for public comment, and the consumer advocacy group says those comments can help save millions.

But in North Carolina, rate review is done privately by the Department of Insurance. Proposed rates are considered trade secrets, not to be disclosed to competitors (and therefore shielded from consumers as well). We'll have to wait until fall, probably October, to see what's in store for folks who buy insurance on the federal exchange.

Meanwhile, a reader sent a link to a Manhattan Institute analysis that appears to forecast huge hikes, with North Carolina facing one of the biggest increases in premiums. "Obamacare To Increase Individual-Market Premiums By Average of 41%," reads the headline on a Forbes piece by Avik Roy, a senior fellow at the Manhattan Institute and former health care adviser to GOP presidential candidate Mitt Romney. North Carolina's increase is listed as 136 percent.

|

| Manhattan Institute map |

|

| Roy |

"In addition, our comparison ignores other differences between pre-Obamacare and post-Obamacare plans," he continues. "For example, in some cases, people looking for comparably-prices coverage on the exchanges will need to accept higher deductibles and other cost-sharing arrangements."

So, is this meaningful data about what has actually happened in North Carolina and across the country? I asked health care experts from UNC Chapel Hill, Winthrop University and the Knight Family Foundation to look at the report and share their thoughts. All were skeptical, not only because of the Manhattan Institute's political agenda but because of the assumptions, extrapolations and proxy measures used in the calculations.

"What this analysis basically concludes is that those who are purchasing lower cost health plans will pay more in premiums for insurance," wrote Winthrop's Michael Matthews and Laura Ullrich, who specialize in health care administration and economics, respectively. "However, you cannot assume any generalizability to the population at large or the average healthcare insurance enrollee. This report simply supports what was already assumed: those who are healthier, younger and in lower cost plans will likely see premiums go up. This is expected when you reduce price discrimination, increase health plan benefits (preventative services) and disallow discrimination based on pre-existing conditions."

Matthews and Ullrich say the data isn't comprehensive enough to conclude that premiums are rising for "the common healthcare consumer."

Jonathan Oberlander, who specializes in health care policy at UNC Chapel Hill, raised similar concerns: "In a system of community rating, where everyone pays the same premium, the young and healthy always subsidize the older and sicker enrollees -- that is how insurance pools work, and it's true as well of employer health plans like the one I am in (state health plan). But the young and healthy will one day be neither young nor healthy, so they will benefit from the system in time as well."

Friday, August 15, 2014

Expert: Pain coming for N.C. businesses, workers

Employees can expect to see more high-deductible health policies as employers try to control costs, a health researcher and former journalist told members of the Charlotte Chamber today.

|

| Connolly |

"It's not a political commentary," said Connolly, a former health correspondent for the Washington Post and author of a book on the Affordable Care Act. "It's pure dollars and cents."

Connolly was a keynote speaker at the Charlotte Chamber's health care summit, which drew about 450 people to the Westin Hotel. The event marked the chamber's Healthy Charlotte fitness campaign and its push to market Charlotte as a national health care destination for patients and businesses.

Hospitals, doctors' offices and other health care businesses employ more than 116,500 people in the Charlotte region and generate more than $6.2 billion in annual wages, the chamber reported.

But Connolly said those businesses lost out on "a serious revenue opportunity" when the state refused the "Obamacare" offer to expand Medicaid coverage for low-income residents with federal money. North and South Carolina are among 21 states that opted not to participate this year, leaving 689,000 low-income N.C. residents in a "Medicaid gap" without coverage.

"Your industries are suffering because you're not getting the increased business," she said.

Update: An editorial in the News & Observer offers more details on the cost of refusing the Medicaid expansion.

|

| Benjamin |

Benjamin, a physician and former Maryland health secretary, told the chamber crowd that federal Medicaid money could have been used to improve mental health services, a need described earlier in the session by Dr. John Santopietro of Carolinas HealthCare System. "The beauty of Medicaid is it is run by the states," Benjamin said. "They can do this. The governors can be creative."

Several local speakers talked about efforts to control health care costs while improving care. Connolly said she expects to see employers take a leading role in coming years. One likely strategy, she said, is a continuing shift to high-deductible policies that hold down premiums by requiring patients to pay a bigger chunk of medical bills from their own pockets. Such policies force employees to think about spending their own money more wisely, Connolly said.

Technology is likely to play a role in helping patients take charge of their own health, from insurance companies offering online cost comparisons to a burgeoning industry in devices that monitor vital signs and exercise, several speakers said. Connolly, who was wearing a wristband that monitors her steps, said she envisions a day when that data would feed to her doctor's office so the doctor would be aware of changes in activity.

Putting insurance in plain English

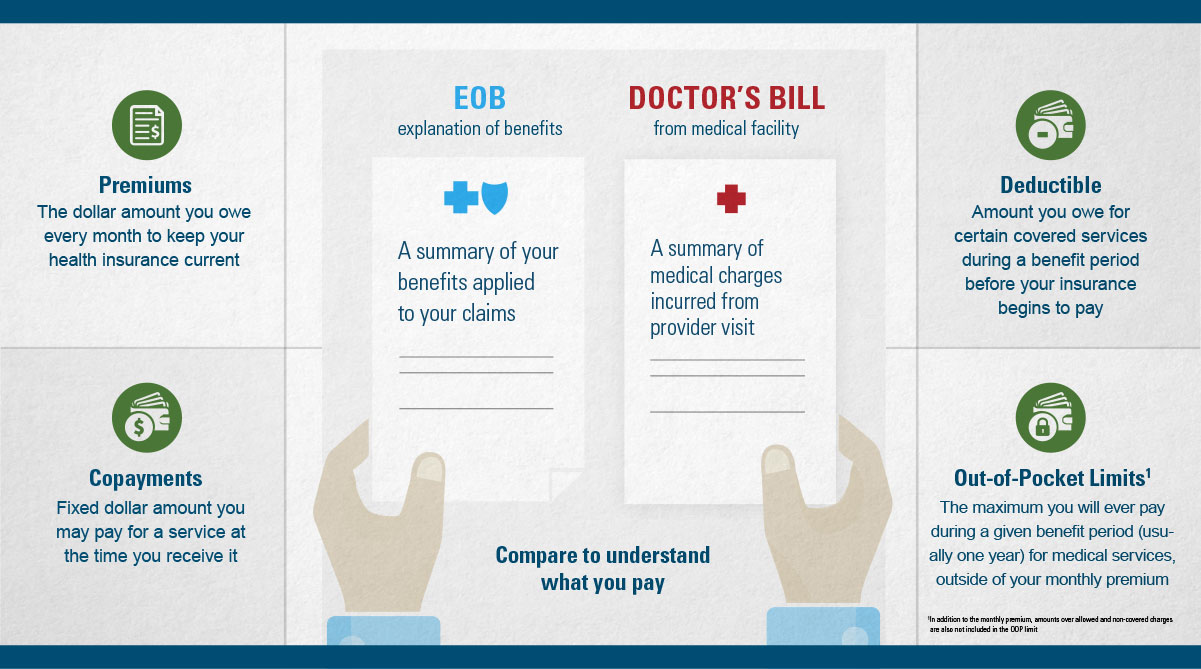

Quick: What's the difference between a copay, coinsurance and cost sharing?

Even if you've had health insurance for years you may hesitate and stumble. And the Affordable Care Act has brought thousands of newcomers into the confusing world of physician networks, deductibles and premium payments.

Blue Cross and Blue Shield of North Carolina, one of two companies offering subsidized policies in our state, has just launched an "Answer Spot" on the company website to help the newly insured take advantage of their coverage. Combined with a 20-page "Welcome Aboard" guide and upcoming open-house events for new customers, it's part of a push to put health insurance in language people can use.

"It really gives you kind of the Cliff Notes version" of a complex subject, says marketing director Bruce Allen.

The guides provide tips on deciphering and paying bills, lining up a primary care physician, understanding insurance networks and figuring out the most effective way to deal with common complaints.

Clear language is always a help, though it won't eliminate all the frustration of navigating the health care maze. Across the country, there are reports of people who rejoiced at getting low-cost insurance, only to learn that the trade-off is a limited selection of doctors and/or significant medical costs that aren't covered. Those of us with employer-sponsored plans have been feeling that pain for years. One of the challenges ahead, for policymakers, researchers and journalists, is teasing out the ways the Affordable Care Act helps or hurts a system that was already struggling with rising costs.

And if you're still puzzling over those definitions: A copay is a fixed dollar amount the patient pays for doctor visits. A deductible is an amount the patient has to pay for certain services before insurance payments kick in; it can range from a few hundred to a few thousand dollars. Once the deductible is met, coinsurance is the percent the patient pays; for instance, insurance may cover 80 percent while the patient pays 20 percent. Cost sharing encompasses all of those, referring to the total out-of-pocket costs.

Friday, August 8, 2014

Obamacare and N.C.: A love-hate thing

Surveys and reports on health insurance and the Affordable Care Act highlight an interesting pattern: North Carolina's elected leaders have done everything possible to avoid participating in "Obamacare," but significant numbers of residents are signing up for subsidized coverage. As the News & Observer's John Murawski recently reported, our state's 357,000 sign-ups during open enrollment ranked us fifth in the nation.

|

| October sign-up in Charlotte |

The Brookings Institution recently offered an interesting hypothesis about political opposition and citizen participation: Anti-Obamacare ads may "backfire" by increasing awareness and enrollment, Brookings fellow Niam Yaraghi wrote in a July report.

|

| Yaraghi |

Thursday, August 7, 2014

Getting started: Confusion, facts and questions

Plunging into health care access has been like going back to college. Since leaving the education beat to take on a new assignment, my head is spinning with new ideas, groups and acronyms (though I confess I haven't read the 2,409-page Affordable Care Act).

I took the Christian Science Monitor's quiz on the act and scored a slightly-above-average 74 percent. (I'm considering this a "before" benchmark.) Mostly I missed questions about other states' standings, though I also overestimated the number of people who lacked health insurance when the act took effect (it's 53 million).

I watched a Jimmy Kimmel video that drove home the need for good information on the topic. His interviews show person after person saying they hate Obamacare but like the Affordable Care Act, unaware that they're two names for the same thing.

I checked out "mythbuster" sites from PolitiFact.com and FactCheck.org. Both mentioned something that was new to me: Members of Congress lost their federal employee insurance and were required to get their insurance through the new marketplaces this year (though they get an "employer contribution" from the federal government).

I sent queries last week to the press offices of Sens. Richard Burr and Kay Hagan and Reps. Robert Pittenger, Patrick McHenry and Richard Hudson asking about their experiences with choosing, buying and using their new plans. Pittenger's press secretary said Pittenger, a Republican who represents the Ninth District, refused to accept the subsidy. But neither he nor any of the others have replied to the questions about their experience. I'll keep trying and let you know what they say.

Even during this slow stretch between open enrollment periods, there's a steady stream of news, polls, studies and opinions about our country's efforts to reshape access to health care. I'll be sharing some of that here for discussion.

But my biggest interest is in what's playing out in real people's lives. Who's getting care and who's hitting roadblocks? What will all this mean for families, businesses and taxpayers? What do readers need to know, as health-care consumers and voters, to move forward?

My contact information is at right, so please share stories that might not work as a blog comment. Readers' tips, comments and questions enriched my education coverage for many years, and I look forward to developing similar relationships here.