Quick: What's the difference between a copay, coinsurance and cost sharing?

Even if you've had health insurance for years you may hesitate and stumble. And the Affordable Care Act has brought thousands of newcomers into the confusing world of physician networks, deductibles and premium payments.

Blue Cross and Blue Shield of North Carolina, one of two companies offering subsidized policies in our state, has just launched an "Answer Spot" on the company website to help the newly insured take advantage of their coverage. Combined with a 20-page "Welcome Aboard" guide and upcoming open-house events for new customers, it's part of a push to put health insurance in language people can use.

"It really gives you kind of the Cliff Notes version" of a complex subject, says marketing director Bruce Allen.

The guides provide tips on deciphering and paying bills, lining up a primary care physician, understanding insurance networks and figuring out the most effective way to deal with common complaints.

Clear language is always a help, though it won't eliminate all the frustration of navigating the health care maze. Across the country, there are reports of people who rejoiced at getting low-cost insurance, only to learn that the trade-off is a limited selection of doctors and/or significant medical costs that aren't covered. Those of us with employer-sponsored plans have been feeling that pain for years. One of the challenges ahead, for policymakers, researchers and journalists, is teasing out the ways the Affordable Care Act helps or hurts a system that was already struggling with rising costs.

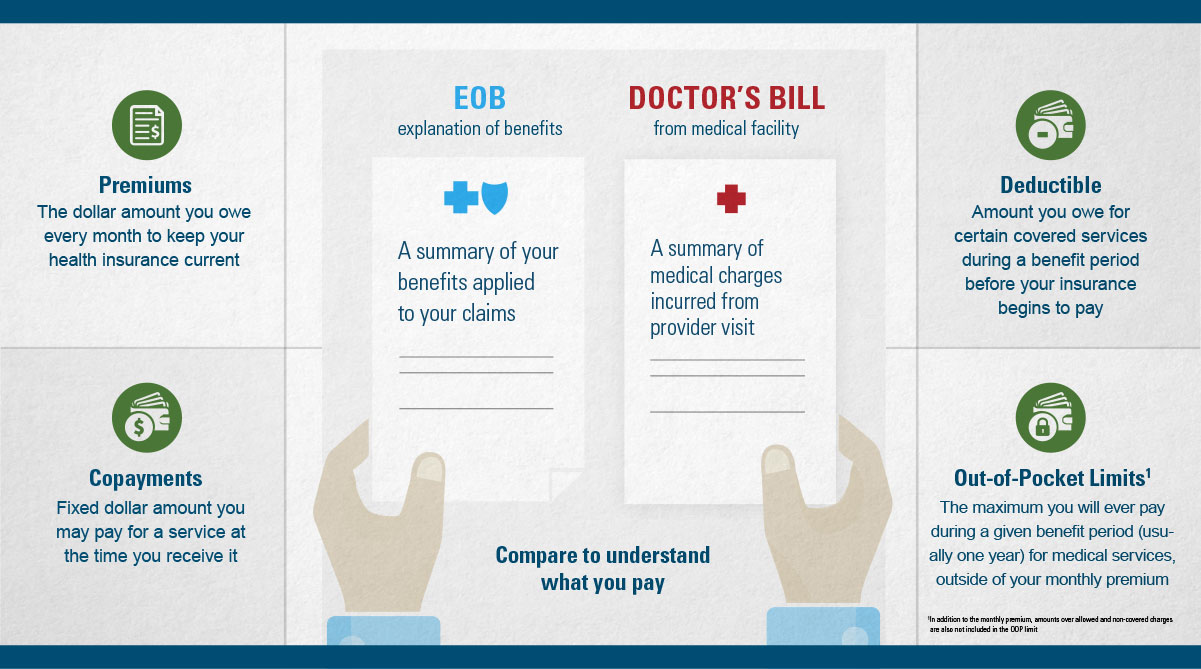

And if you're still puzzling over those definitions: A copay is a fixed dollar amount the patient pays for doctor visits. A deductible is an amount the patient has to pay for certain services before insurance payments kick in; it can range from a few hundred to a few thousand dollars. Once the deductible is met, coinsurance is the percent the patient pays; for instance, insurance may cover 80 percent while the patient pays 20 percent. Cost sharing encompasses all of those, referring to the total out-of-pocket costs.

3 comments:

Is she this ignorant no have known all this before?

Doesn't seem to know much about Obamacare. I got a 260% increase to $450 a month with a $5500 deductible. That's almost $11,000 per year before insurance kicks in. Where do I get the $11,000?

Thomas, I'd love to talk to you more about your experience for future stories. My contact info is at right. Not clear to me whether you're on an individual policy or workplace, but interested either way. High deductibles are a big issue, though it's not clear how much of that is attributable to ACA vs. general rising costs.

Post a Comment